Nexus Sums Up Bangkok’s Property Market in 2019

Steady Condo Market With Good Absorbtion Rate

Office Buildings, Shopping Malls Keep Growing

(25 December 2019 : Bangkok) Nexus cites the average condominium price in Bangkok went up 1%, marking the lowest growth over the past 5 years, while the sale rate shrank 17%. It is anticipated that developers will focus more on real demand over the next two to three years. The rental rate of Grade A office in CBD area kept increasing constantly, whereas the rental rate of Grade A shopping mall rose up to 3,915 baht per square meter per month and tends to further increase. The markets of office buildings and shopping malls will face higher competition. The government’s incentive plans will be the key factor to determine the growth of property market.

Condominium Market

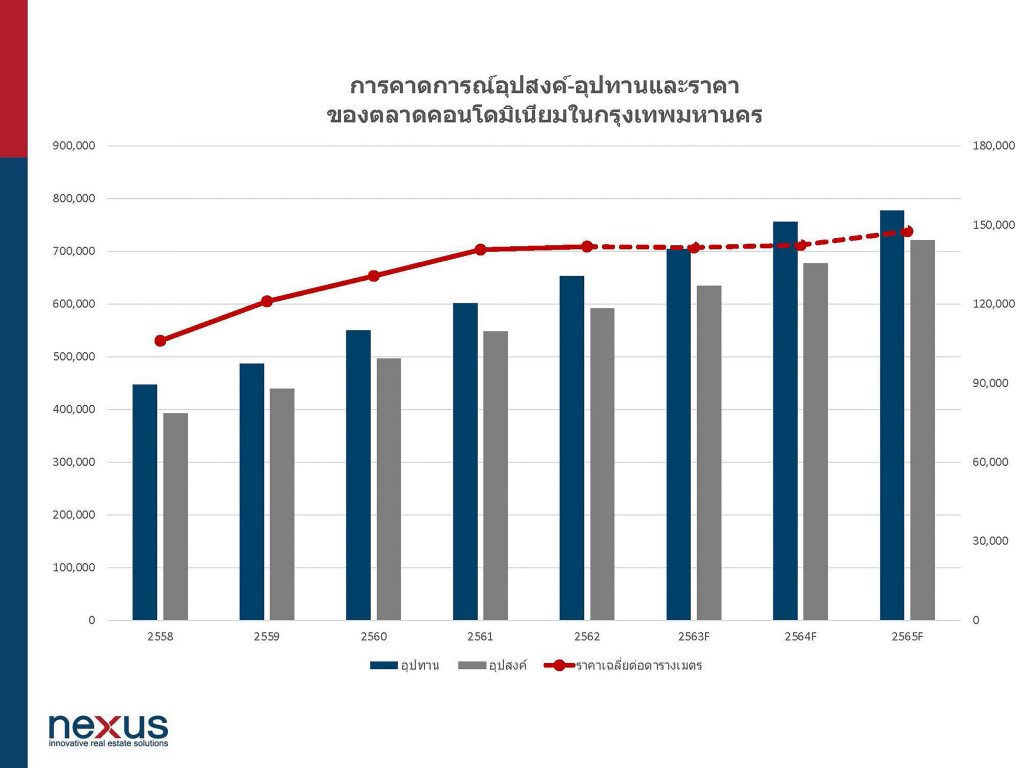

Mrs. Nalinrat Chareonsuphong, Managing Director of Nexus Property Marketing Company Limited, says that supply in condominium market has declined by 29% from 2018. There were new supply of 43,000 units from 126 projects, resulting in total cumulative supply of 654,200 units. Developers shifted to focus on the extension of new mass transit lines including the MRTA Blue Line on Thonburi side, the Green Line Extension to the north and the Yellow Line. It was found that the highest new supply was in the Thonburi / Petchkasem area (10,100 units, 23%), followed by the Phra Khanong / Suan Luang area (7,800 units, 18%) and the Ladprao / Wangthonglang area (6,100 units, 14%), respectively. Considering the overall market, it indicated the growth rate of new supply in the Thonburi / Petchkasem was the highest, more than 63% over the past 5 years. The main reasons were related to inexpensive land price and extension of mass transit system projects.

To analyze new supply this year, the market experienced the big change in selling products. Almost 50% of total new supply was in the mid-market, priced between 75,000-110,000 baht per square meter, surging from 27% last year. This reflects that developers focused the potential of real demand in condominium market in Bangkok and developed their products in respond to buyer’s purchasing power. Many projects adjusted the price strategy or even paused the sale activity after the project launch to readjust the price or revise the products accordingly. Another interesting point is a sharp drop-off in hi-end market as the ratio of new projects was only 22% in 2019, compared to 40% in 2018. Meanwhile, the ratio of new development in city-condo, luxury and super luxury remain unchanged from last year.

In terms of sales, the year 2019 recorded total sales of condominium in Bangkok at 43,200 units. Of total, new supply in 2019 accounted for 20,700 units (average sales at 48%) and supply before 2019 recorded 22,500 units. The sales this year boosted the gross sales rate of overall market to 90% and there were 62,700 units remaining in the market. However, the sales rate declined 17%, still lower than the decelation rate of new supply.

It showed a better sign of the absorption rate. However, the sales would be in a better condition if the market had not suffered with the the government’s LTV measures and the appreciation of baht, dumping demand from foreigners.

Source: Nexus Research, December 2019

In 2019, the average condominium price slightly increased by 0.9% from 140,600 baht per square meter to 141,800 baht per square meter. This is considered very low, compared to the rate adjustment over the past 5 years at 8% per annum on average. The city-centered market has adjusted to real demand. The average price of newly opened projects this year was 15% lower than the one in 2018. Consequently, the average price of city-centered market was maintained at 231,300 baht per square meter. The area around the city’s center was up 1% to 114,400 baht per square meter, while the outer-ring market surged 3% to 76,000 baht per square meter.

For the investment angle, it is found that condominium projects in Bangkok were mainly invested by two groups of investors: foreign institutional investors and Thai developers. For the first group, they were mostly from China and Japan, focusing on the hi-end market. The investment from this group represented 29% of total market. The difference between the Chinese and the Japanese investors is that the Chinese invest independently, whereas the Japanese prefer a joint venture with Thai listed companies. For Thai developers, it is found that the proportion between small developers and listed ones is around 30:70. However, more small developers kept entering into the market with focusing on smaller projects.

Forecast 2020

For the trend of condominium market in 2020, Mrs. Nalinrat believes that the number of new supply should increase around 42,000-45,000 units, similar to 2019. Some of them are the projects that were delayed the development from 2019. However, if the government’s LTV measure remains the same, demand will also be similar to 43,000-48,000 units in 2019, the gross sale rate will stand at 90% and the unsold units will be around 60,000 units. The price in 2020 should slightly decline in some areas especially in the first half of the year. Price of new products will be controlled to meet the real demand, allowing investors to buy condominiums in reasonable price.

Over the past years, the factors that make condominium market grow continuously were 1. Demand in new locations due to the extension of mass transit system 2. Domestic property investment market 3. Surging land price and 4. Purchasing power from foreigners. In 2019 and 2020, the overall market would not be much expanded because the investment would be slowdown by LTV measures, land price is constant and investors become more cautious to buy land. In addition, if the baht keeps strong, investment from foreigners will not increase either. The only positive factor should be the completion of the extension of mass transit, making the commuting more convenient and expanding new areas for development.

The government has been trying to launch the policies to stimulate demand in the real estate sector, for example, the reduction of transfer fee or the return of down payment. However, LTV measure is the main factor that retards the market growth because consumers faced the obstacle to get the loan. In addition, the uncertainty in property valuation for land and building tax, which will be effective next year, delayed investors’ decision. Nevertheless, the government’s measures should be able to stimulate the demand in the fourth quarter of 2020. If the government wants to accelerate the market growth, it should ease LTV measure and reduce the transfer fee without the price ceiling.

For location, it is found that the attractive locations are the area where the extension of mass transit system is completed. Existing projects that have not been sold out shoud gain benefits. Meanwhile, the mass transit system lines that are under construction, for example, Yellow Line, Pink Line and Orange Line have the chance to grow because those extension areas still have demand and the land price is not very expensive. These areas are suitable for mid-market and city-condo market.

For Smart City and the effort of developing residential projects by combining technology, infrastructure and services, most of them are large-sized mixed-use projects and are collaborated between the public and the private sector. There are 3 main factors for these projects, which are existing community, transit system that links between the projects, and amenities and services. In long term, the development of Smart City will stimulate the economic growth in local community and spread the growth continuously.

Currently, several developers have announced the mega-projects. Meanwhile, the government itself held the bidding for a plenty of potential land plots, for example, Makkasan land or Klongtoey Port Land under the concept of Smart City. Those land plots are larger than 100 rais, so the projects need to accommodate several components especially the main part should be commercial spaces.

Office Market

Mr. Teerawit Limthongsakul, Managing Director of Nexus Real Estate Advisory Company Limited, says the office market in Bangkok, with total space of 9 million square meters, of which Grade A and B buildings accounted for 6.08 million square meters, still remains growing constantly. Due to higher rental cost and low space vacancy rate for several years, there are more development of the office buildings. It is forecasted that there will be new supply of 1.78 million square meters in the next five years.

The overall occupancy rate in Bangkok is approximately 94% and the overall rental rate is approximately 800 baht per square meter per month. For Grade A office building in the central business district (CBD), the rental price has revised up 5% from end of last year to 1,080 baht per square meter per month and the occupancy rate is at 95%, slightly higher than the overall rate. According to the survey, there are still high demand for Grade A office building in CBD area, spiralling up the price, for example, Gaysorn Tower that records the most expensive rental price at 1,600 baht per square meter per month. Ploenchit, Rama 1 and Wittayu also gain high attention from tenants continuously.

Source: Nexus Research, December 2019

Since most of office buildings in Bangkok are over 20 years old, the upcoming supply will interestingly refresh the market. Most of new projects are developed as mixed-use projects, contributing the low floors as retail space to support and provide convenient services to tenants. From 2022 onwards, several large projects will be completed, for example, Supalai Icon on the land of former Australia Embassy, One Bangkok from TCC, The Forestia – the country’s first city in the forest project, Bangkok Mall from The Mall Group and M Sphere – the last jigsaw piece of The M District. All of them will enhance the standard of office building in Thailand.

Retail Space Market

Although the household debt in Thailand remains high and the consumer confidence index slightly decreases, foreigners’ spending still supports the growth of retail market. In the second half of 2019, the number of foreign tourists and the income from foreign tourists increased. Chinese are the majority of foreign tourists in Thailand. In addition, the six-month extenstion of the exemption of Visa on Arrival fee, the prolonged protest in Hong Kong, and the tax increase in Japan were main reasons supporting the increase of foreigner tourists. Ministry of Tourism and Sport’s statistic showed that there were 29.47 million foreign tourists in the first nine months of the year, up 3.51% from the same period in the previous year, and the income made from foreign tourists totalled 1.42 trillion baht, growing 3-4% year on year.

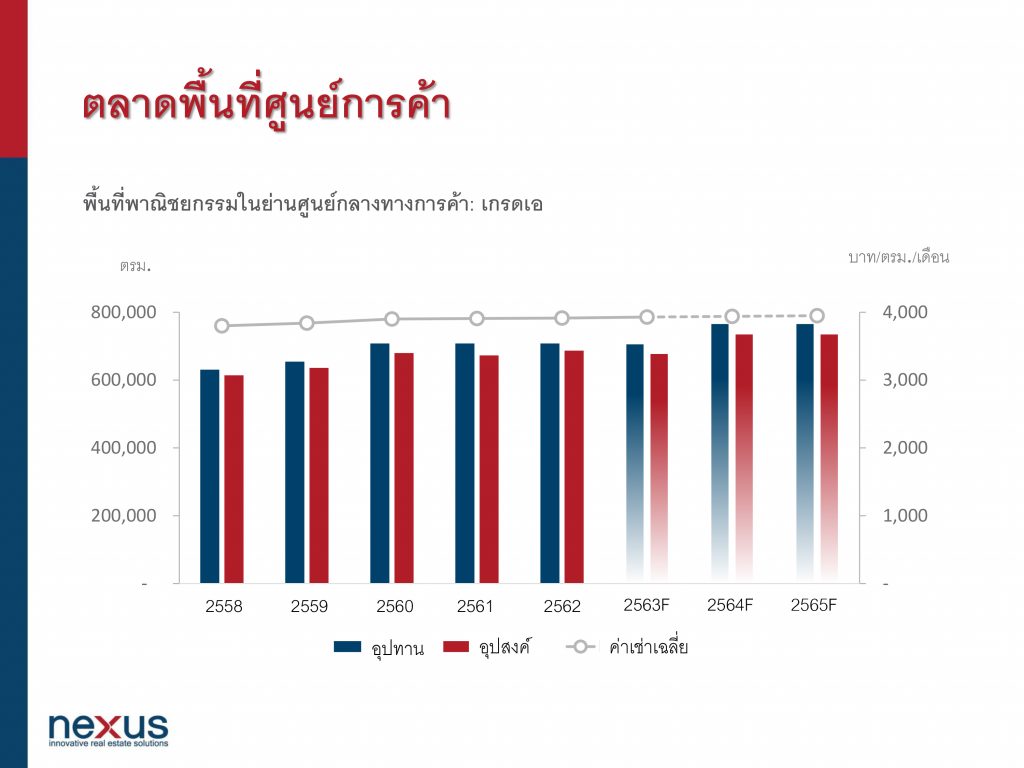

The survey found that the shopping mall space market still grows constantly and the rental price remains high especially in the commercial area like Siam, Rajprasong, and Phromphong. These commercial areas are the significant destination of foreign tourists who have high purchasing power. This results to the high occupancy rate, over 95%, of the retail properties.

High competition at present makes more shops and shopping mall entrepreneurs bargain the rental in term of Gross Profit (GP) sturcture . Large shopping malls offers fix minimum guarantee or based rent with tenants, indirectly forcing tenants to find the way to boost sales. From the survey, it is found that the average rental fee on G Floor in shopping mall costs around 3,915 baht per square meter per month, slightly higher than last year.

However, shopping mall operators need to face the challenge from the changing behavior of consumers. Online shopping, rapidly growing food delivery and new supplies are sharing the purchasing power. These forces the operators to create new experiences to consumers. Meanwhile, Thai brands also encounter fierce competition from foreign brands, tapping into Thai market continuously, for example, Donki Mall, Tim Horton, Yi Fang, Taco bell, Tiger Sugar, The Alley, and Xing Fu Tung.

In 2019, the commercial space market had new supply of over 280,000 square meters, for example, 101 the third place, Don Don Donki, The Market Bangkok, Samyan Mitrtown, Central Village, and I’m Chinatown. It forecast that there will be at least 400,000 square meters of new supply over the next three years. The interesting projects will include M Sphere, One Bangkok and Siam Premium Outlets Bangkok.

Source: Nexus Research, December 2019

In conclusion, the retail market in Bangkok remains attractive and is likely to grow continuously. However, it is necessary for operators to build new experiences that consumers cannot get from online or delivery service. They should be able to meet customer satisfaction and provide quick service while maintaining the relationship with customers and always developing the products.